If you're managing more than a handful of properties, you already know the basics. You know income has to be tracked, expenses documented, and owners paid on time. The problem isn't knowledge - it's that the system you're using wasn't built for how short-term rentals actually work.

OTA payouts don't match individual reservations. Month-end takes days instead of hours. An owner calls with a question and you need five minutes and three spreadsheets just to give them a straight answer. The books technically reconcile, but you're not confident you'd pass an audit.

This guide is for property managers who are past the beginner stage and hitting the ceiling of manual processes. We cover the specific accounting challenges that emerge at 10, 20, and 50+ properties, and walk through how to build systems that scale without adding more manual work. Use the links throughout to go deeper on any topic.

Importance of Accurate Accounting in Short Term Rentals

Accurate accounting serves to establish a solid foundation for tax reporting and compliance. Mistakes or oversights can lead to penalties, audits, or other legal issues that could jeopardize your rental business. Hence, implementing a robust accounting system from the onset is imperative for long-term success. In addition to compliance, accurate records can also enhance your ability to secure financing or investment opportunities. Lenders and investors often require detailed financial statements to assess the viability of a rental property, making it essential to maintain meticulous records of income, expenses, and overall financial health. This diligence not only supports your current operations but also positions your business favorably for future growth and expansion in the competitive short term rental market.

Key Principles of Short Term Rental Accounting

To effectively manage short term rental finances, it is essential to adhere to several key accounting principles. These principles not only provide structure but also foster transparency and credibility in your financial activities.

Revenue Recognition in Short Term Rentals

Revenue recognition is a fundamental accounting principle that defines when and how income is recorded. For short term rentals, revenue must be recognized when the services are rendered, namely, when guests check into the rental property. This ensures that income reflects the actual booking period. A report from the American Institute of CPAs emphasizes the importance of adhering to this principle to avoid discrepancies in financial reporting.

Additionally, it’s important to account for cancellations and refunds properly. Adjusting revenue figures for these instances can provide a clearer financial picture and help prevent overestimating your income. Furthermore, implementing a robust cancellation policy can mitigate the financial impact of last-minute cancellations, allowing owners to maintain a more stable revenue stream.

Expense Tracking and Management

Expense tracking is another critical component of short term rental accounting. Owners should document all expenses, including maintenance costs, cleaning fees, utilities, and property management fees, to have an accurate representation of their financial health. A study by the Institute of Real Estate Management found that effective expense tracking can lead to a 15% reduction in unnecessary costs.

Want every expense connected to the right reservation and automatically included on owner statements? See how this works in VRTrust

Moreover, utilizing a systematic approach to categorize these expenses can simplify the management process. Consider using accounting software or spreadsheets to keep track of your expenditures, making it easier to analyze and identify potential areas for savings. Regularly reviewing these expenses can also lead to better budgeting practices, allowing owners to allocate funds more effectively for future improvements or unexpected repairs. In addition, understanding seasonal fluctuations in expenses can help in planning for peak rental periods, ensuring that properties remain competitive and well-maintained.

Navigating Tax Implications for Short Term Rentals

Understanding and managing tax implications is crucial for short term rental owners. Failing to comply with tax obligations can result in significant financial repercussions, so being informed is key.

Understanding Rental Income Tax

Rental income tax refers to the taxes levied on the various income streams generated from your rental properties. In the United States, for instance, profits made from short term rentals are generally considered taxable income and must be reported on your tax return. According to the IRS, failing to report rental income can lead to penalties and interest on unpaid taxes.

It's also important to understand your local tax laws as they can vary significantly. Some jurisdictions impose additional transient occupancy taxes specifically for short term rentals. Ensuring compliance can save you from hefty fines and legal troubles. Moreover, some areas may have specific regulations regarding the number of days a property can be rented out on a short-term basis, which can directly affect your income and tax obligations. Staying updated on these regulations is essential for maintaining a successful rental operation.

Exploring Deductible Rental Expenses

On the upside, many of the costs associated with managing a short term rental can be deducted from your taxable income. This includes maintenance costs, property management fees, advertising expenses, and even depreciation of the property itself. A report from the National Association of Tax Professionals highlights that many rental owners miss out on significant deductions simply due to lack of awareness.

Being detailed and organized in tracking these expenses will not only assist in tax preparation but will also enhance your overall financial strategy. Additionally, consulting a tax professional can provide tailored advice relevant to your specific circumstances. Beyond the standard deductions, you might also consider the benefits of investing in energy-efficient appliances or smart home technologies, which can qualify for additional tax credits. These improvements not only attract more guests but can also lead to lower utility costs, creating a win-win situation for your rental business.

Implementing Effective Bookkeeping Strategies

Implementing effective bookkeeping strategies is indispensable in maintaining the financial health of your short term rental. With the right tools and approach, you can streamline your accounting practices and save time. This not only helps in ensuring compliance with tax regulations but also provides a clear picture of your financial standing, enabling you to make informed decisions about future investments or improvements to your property.

Choosing the Right Accounting Software

In the digital age, there are numerous accounting software solutions tailored for rental management. Choosing the right software can simplify your bookkeeping, allowing you to track income, expenses, and profits in real-time. An effective software solution can also automate repetitive tasks, such as invoicing and payment reminders, freeing up your time to focus on enhancing guest experiences. Research from Software Advice indicates that 70% of property owners who use accounting software report improved financial management.

Some popular options include QuickBooks, FreshBooks, and Xero. When selecting software, consider factors such as user-friendliness, integrations with rental platforms, and the ability to generate financial reports. The right tool aligns with your business needs and enhances efficiency. Additionally, many platforms offer mobile applications, enabling you to manage your finances on the go, which is particularly beneficial for busy hosts juggling multiple responsibilities.

Regular Financial Reporting and Analysis

Regular financial reporting is essential for keeping tabs on the performance of your short term rental. Monthly or quarterly reports can help you assess profitability, identify trends, and adjust your strategies accordingly. By maintaining a consistent schedule for these reports, you can quickly spot any discrepancies or unexpected expenses that may arise, allowing you to address issues before they escalate. A study by the Institute of Real Estate Management found that properties with regular financial reviews perform better in terms of profitability.

Beyond just collecting data, analysis plays a crucial role. Utilizing key performance indicators (KPIs) such as occupancy rate, average daily rate, and gross rental revenue can provide valuable insights into your business. These metrics allow for data-driven decision-making, ultimately improving your rental operations. Moreover, comparing your performance against industry benchmarks can help you understand where you stand in the competitive landscape, guiding you in setting realistic goals and identifying areas for improvement. Engaging with financial advisors or accountants who specialize in the rental market can further enhance your understanding and application of these metrics, ensuring you are making the most of your rental investment.

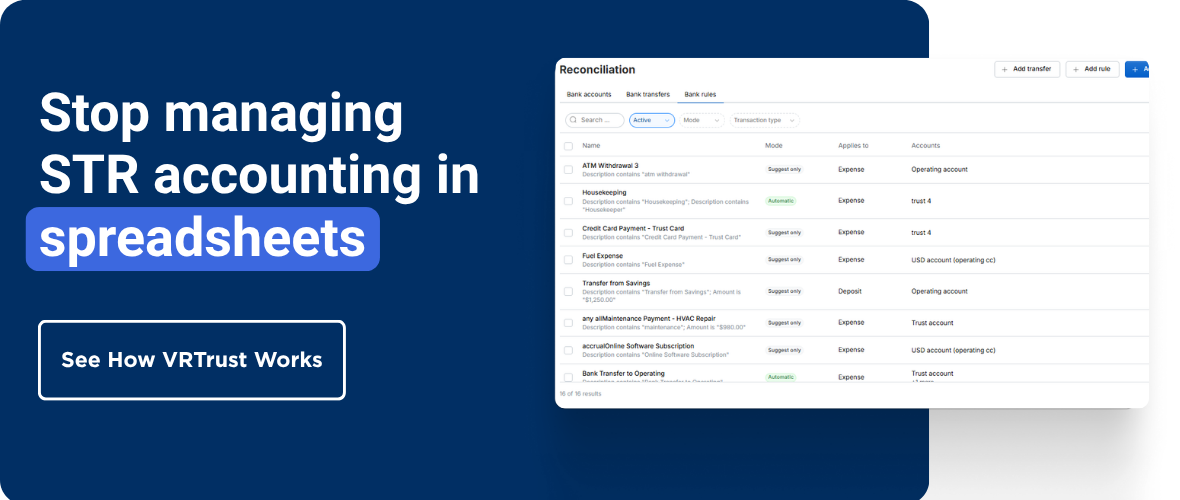

Common Bookkeeping Nightmares — And How STR Managers Fix Them

Most short-term rental accounting problems aren't caused by ignorance. They're caused by systems designed for a simpler business model hitting the complexity of vacation rentals. Here are the five most common ones and what actually fixes them.

Nightmare 1: OTA Batch Payouts That Won't Reconcile

Airbnb deposits a single lump sum covering six reservations, three properties, two owners, and a disputed chargeback. Your accounting software sees one transaction. You spend an hour working backward.

The fix: Stop reconciling from the bank and start from the reservation. Pull the OTA transaction detail report first, allocate each reservation to its owner and property, then match the sum to the bank deposit. Better yet, use software that does this automatically by pulling reservation-level data directly from Airbnb and Vrbo.

→ How to Generate Reconciliation Reports

Nightmare 2: Month-End That Takes a Full Week

Closing the books for 20 properties shouldn't consume your entire first week of the following month. But it does when every step is done manually, from reconciling bank activity and categorizing transactions to splitting fees and building owner statements.

The fix: Implement a continuous close process. Reconcile weekly rather than monthly. Set up automated rules for recurring transactions. By the time the calendar flips, 80% of the work is already done.

→ Continuous Close Checklist for STR Property Managers

Nightmare 3: An Owner Calling About Their Balance

"What's my balance right now?" should take ten seconds to answer. If it takes more than ten minutes, your system isn't built for trust accounting.

The fix: Every owner should have a live ledger balance that updates in real time as reservations are confirmed, expenses are posted, and deposits clear. This isn't a reporting feature: it's the core output of proper trust accounting. If you can't answer that question instantly, the architecture of your accounting system needs to change.

→ What Is Trust Accounting and Why Vacation Rental Managers Can't Ignore It

Nightmare 4: Records That Have Zero Audit Trail

If a bank or regulator asked you to produce trust account reconciliations for the past 18 months, how long would it take? If the honest answer is "I'd have to piece it together," that's not a good sign.

The fix: Every reconciliation should be date-stamped, signed off by a named team member, and stored in a retrievable format. Three-way reconciliation between your bank balance, book balance, and sum of owner ledgers should be captured in one place, not spread across your PMS, spreadsheets, and email.

→ How to Generate Trust Compliance Reports

→ How to Generate Audit-Ready Reports

Nightmare 5: Tax Season Catching You Off Guard

1099s need to go out. You need to know how much each owner earned. Your accountant needs a clean general ledger. And you're realizing none of your records are in the format they need.

The fix: Year-end should require almost no work if you've been accounting correctly all year. Each owner's income should be visible from their ledger at any time. Set up your chart of accounts in January so that every category your accountant needs is already tracked.

→ How to Prepare 1099 Forms for Property Managers

→ How to Generate Year-End Owner Summaries

Legal Considerations in Short Term Rental Accounting

Lastly, staying compliant with legal regulations surrounding short term rentals can be complex but is absolutely essential. Each jurisdiction has its own rules that landlords must adhere to, and understanding these laws is part of responsible ownership.

Complying with Local and State Regulations

Before starting your short term rental business, it is vital to familiarize yourself with local and state regulations. This includes licensing requirements, safety codes, and zoning laws specific to short term rentals. A report from the Urban Land Institute indicates that 40% of short term rental owners are unaware of the specific regulations in their area.

Moreover, some cities have specific limits on the number of days a property can be rented short-term, or they may impose restrictions on the types of properties that can be listed. Non-compliance can lead to serious penalties, including fines or the revocation of your rental permit. Therefore, diligent research and adherence to these regulations are essential for smooth operations.

Understanding Legal Obligations as a Short Term Rental Owner

In addition to local regulations, short term rental owners should be aware of their legal obligations, such as respecting tenant rights, ensuring property safety, and providing accurate property descriptions in listings. Transparency and honesty in your rental operations foster trust with guests and help mitigate potential disputes. A survey by the National Association of Realtors found that properties with clear communication and transparency have a 20% higher guest satisfaction rate.

Ultimately, understanding and managing both the financial and legal aspects of short term rentals will allow you to navigate this unique market effectively and sustainably. By mastering short term rental accounting, you can focus on what truly matters: providing a great experience for your guests and maximizing your rental income.

Everything You Need: STR Accounting Resource Index

Use this index to navigate to the specific topic you need. Each link goes deeper on a single area of short-term rental accounting.

Financial Reports

- The Complete List of Financial Reports for Property Managers →

- Financial Reports Guide for STR Property Managers →

- How to Generate Income Statements →

- How to Generate Profit and Loss Statements →

- How to Generate Revenue vs. Expenses Summaries →

- How to Generate KPI Dashboards →

- 4 KPIs for Vacation Rental Accounting →

Owner Statements & Payouts

- Owner Statement & Payout Guide for STR Managers →

- Why Manual Owner Statements Are Costing You Clients →

- How to Generate Owner Statements →

- How to Generate Monthly Owner Statements →

- How to Generate Year-End Owner Summaries →

- Accounting and Owner Statement Tips for Hostfully Users →

Trust Accounting & Compliance

- What Is Trust Accounting and Why Vacation Rental Managers Can't Ignore It →

- Basics of Trust Accounting for Vacation Rental Managers →

- Why Trust Accounting Is the Secret Competitive Edge →

- Compliance & Audit Reports Guide →

- How to Generate Trust Compliance Reports →

- How to Generate Trust Account Statements →

- How to Generate Audit-Ready Reports →

- Continuous Close Checklist for STR Property Managers →

Reconciliation

- How to Generate Reconciliation Reports →

- How to Generate General Ledger Exports →

Tax & 1099s

- How to Prepare 1099 Forms for Property Managers →

- How to Generate 1099 Summaries →

- Tax Reporting Tips for Vacation Rental Property Managers →

Tools & Software

- Best Accounting Software for Vacation Rental Managers (2026) →

- QuickBooks Alternatives for Short-Term Rental Accounting →

- VRTrust vs. QuickBooks Online →

- How to Transition from QuickBooks or Spreadsheets →

Ready to take the next step in mastering your short term rental accounting?

Most accounting systems weren’t designed for the operational complexity of vacation rentals. VRTrust brings together trust accounting, owner statements, reconciliations, and financial reporting in one system — giving teams greater visibility and control as they scale.

Embrace efficiency and make informed decisions with ease, enhancing trust and customer loyalty while paving the way for business growth. Don't miss out on the opportunity to scale your operations with ease. Sign up for a free trial today!