Three-Way Reconciliation for Vacation Rental Property Management

Without regular reconciliation, property managers can lose visibility into what’s actually happening in their owner accounts. Even small discrepancies can grow over time, leading to messy month-end closes, confusing owner statements, and hours spent tracking down issues after the fact. Regular reconciliation helps catch problems early, before they become difficult and time-consuming to untangle.

More than just accounting jargon, three-way reconciliation is the process that helps property managers verify that their numbers are accurate.

Trust accounting adds another layer of complexity because you're not just tracking your own money. You're tracking money that belongs to multiple owners and guests across dozens to hundreds of reservations. Guest deposits, owner reserves, pending payouts, and withheld expenses all flow through the trust account, and you need confidence that your owner balances and payouts are accurate at any given time.

This guide breaks down the entire process, from understanding the three balances that must match to handling the specific challenges that vacation rental managers face daily.

What is Three-Way Trust Account Reconciliation?

Reconciliation: The Basic Definition

Reconciliation is the process of comparing two or more records to ensure they agree. Bank reconciliation, the most common form, compares your internal records to your bank statement. You're looking for transactions that appear in one place but not the other: checks that haven't cleared, deposits in transit, or errors that need correction.

Trust account reconciliation follows the same principle but applies it to accounts holding other people's money. The purpose of separating owner funds from operating funds is to keep financial records clean, accurate, and easy to follow, especially as transaction volume grows.

The Three Balances That Must Match

The "three-way" in three-way reconciliation refers to three distinct balances that must equal each other:

- The adjusted bank balance (your bank statement balance, modified for outstanding items)

- The ledger balance in your accounting system (what your books say you have)

- The sum of all individual owner and guest balances (what you owe to each party)

Think of it like a restaurant where every table has a separate tab. The cash in the register should equal what your point-of-sale system shows, and that should equal the total of all open tabs. If any of these numbers disagree, something is wrong.

The Importance of Trust Reconciliation in the Vacation Rental Industry

Vacation rental management creates unique reconciliation challenges. Unlike traditional property management with monthly rent payments, short-term rentals involve constant transaction flow. A single property might have twenty reservations per month, each with deposits, cleaning fees, taxes, and owner payouts.

In states where short-term rental accounting is highly regulated, property managers are required to reconcile trust accounts and prove they are accurate. Beyond compliance, though, accurate reconciliation helps property managers stay organized, maintain clear owner reporting, and maintain a trustworthy reputation. Owners want to see exactly where their money is, and they want those numbers to be correct. (See our article on trust accounting as a competitive advantage.)

Trust Account Reconciliation Basics for Vacation Rental Managers

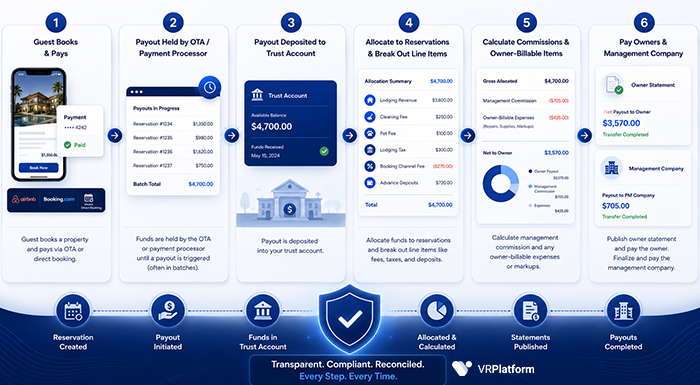

Typical Flow of Funds

Understanding how funds flow is essential before attempting reconciliation. Here's how money typically moves through a vacation rental trust account:

- A guest books a property and pays through Airbnb, Booking.com, or a direct booking. The payment sits with the OTA or in your payment processor until a payout is triggered (this often occurs in batches combining payouts for multiple reservations)

- These funds are deposited in your trust account

- From that gross amount, you need to allocate each portion to the appropriate reservations and break out line items like booking channel fees, cleaning fees, pet fees, and lodging taxes collected

- Next, you calculate management commission and any owner-billable expenses or markups

- Owner statements are published, and the net payout is transferred to the owner

- Lastly, finalize and transfer the total amount payable to the property management company

Since funds might arrive days or weeks after a reservation is booked, timing can create complexity, and your reconciliation process must account for this.

Handling Guest Deposits and Payments

Guest payments rarely arrive as clean, individual transactions. OTAs batch multiple reservations into single deposits, sometimes combining payments from different properties and different owners. A $3,500 deposit might represent five separate reservations across three properties.

Your accounting system needs to unbundle these deposits and allocate each portion to the correct reservation and owner. This allocation is where many reconciliation problems begin. If you don't properly match incoming funds to specific reservations, your owner balances will be wrong even if your bank balance is correct.

Understanding Guest Balances (a.k.a. Accounts Receivable)

Accounts receivable in vacation rental management represents money guests owe but haven't yet paid. This occurs with direct bookings that allow payment at check-in, installment payment plans, or reservations where the balance is due closer to arrival.

These receivables affect reconciliation because they represent future payments that haven’t arrived yet. Your system needs to track what's owed versus what's received, and your financial reports should distinguish between earned revenue and collected revenue.

Factoring in Expenses, Commissions, and Fees

Every reservation generates multiple financial events beyond the guest payment. Your management fee might be a percentage of the base reservation fee. Cleaning fees might go to the property manager or to the owner. Merchant processing fees reduce the net amount. Property-specific expenses like repairs or supplies get deducted from the owner payout.

Each deduction changes the owner's balance. If you charge a $150 repair to an owner's account, their balance decreases by that amount. Your reconciliation must capture every adjustment, not just the major payment transactions.

A Step-by-Step Guide to Three-Way Reconciliation

Adjust the Bank Balance for Outstanding Items

Start with your bank statement ending balance. This number represents cleared transactions only. It doesn't include checks you've written that haven't been cashed or deposits that haven't posted.

Create a list of outstanding items: owner payout checks that haven't cleared, deposits in transit, and any bank errors you've identified. Add deposits in transit to the statement balance and subtract outstanding checks. The result is your adjusted bank balance.

For example, if your statement shows $50,000, you have $3,000 in outstanding checks and $2,500 in deposits that will post tomorrow, your adjusted balance is $49,500.

Reconcile to Cash

Your accounting system maintains a cash balance for the trust account. This balance should reflect all transactions you've recorded, regardless of whether they've cleared the bank. Pull your general ledger balance for the trust account as of the same date as your bank statement.

Compare this ledger balance to your adjusted bank balance. They should match. If they don't, you have unrecorded transactions or errors. Common culprits include bank fees you haven't entered, guest refunds, or duplicate entries.

Work through each discrepancy until the two balances agree. This is the first reconciliation of your three-way process.

Verify Account Balances Match

The third balance is the total of all individual balances tracked within the account. This includes amounts owed to owners, guest deposits or prepaid balances being held, and any property management revenue that has not yet been transferred to the operating account.

If all three match, your reconciliation is complete. You can prove that every dollar in the trust account belongs to a specific party and that you have enough cash to pay everyone.

When the balances don't match, you need to investigate. The difference might be an owner payment recorded incorrectly, a reservation allocated to the wrong property, or an expense that wasn't assigned to any owner.

Transfer Money from the Trust Account

Once reconciled, you can confidently publish owner statements, process owner payouts and transfer the portion owed to you as the property manager to your operating account. The reconciliation proves you have sufficient funds to pay each owner their balance and cover your management fees.

Managers should reconcile before every payout cycle. This prevents the nightmare scenario of paying an owner money you don't actually have, which can create confusion, cash flow issues, and difficult owner conversations.

Common Reconciliation Issues in Short-Term Rentals

OTA Batch Deposits

OTA batch deposits are the single biggest reconciliation headache for vacation rental managers. Airbnb might send you one deposit covering twelve reservations, and the deposit amount doesn't match the sum of the individual reservation totals due to adjustments, resolutions, or timing differences.

Proper reconciliation requires breaking down each batch deposit and matching it to specific reservations. Your software should support this unbundling process. Without it, reconciliation quickly becomes manual and difficult to manage at scale.

Refunds and Adjustments

Guest refunds create reverse transactions that can impact reconciliation. If you refund $500 to a guest, that money leaves your trust account, and the associated guest or owner balance should decrease accordingly, depending on whether you recognize revenue at booking or at check-in.

Partial refunds, OTA-initiated refunds, and chargebacks each have different accounting treatments. Some reduce owner revenue; others might be absorbed by your management company. This is why it’s important to check for any cancelled or unpaid reservations during reconciliation to ensure they don’t go unnoticed.

Expense Allocation by Property

When you pay a vendor, restock supplies, or incur some other expense for a property, you need to allocate it correctly. Consider a landscaper who maintains three properties, but sends one invoice. That single payment must be split across three owner accounts in the correct proportions.

Misallocated expenses create reconciliation differences that are hard to find. Owner A shows a higher balance than they should, while Owner B shows less. The total might still be correct, but the individual balances are wrong. This is where it comes in handy to have a system that allows you to allocate individual expense lines to different accounts.

Best Practices for Vacation Rental Reconciliation

Frequency and Timing of Reconciliation Reports

Most property managers reconcile monthly, though teams with higher transaction volume may reconcile more frequently.

The right frequency depends on your volume and risk tolerance. More frequent reconciliation catches errors faster, when they're easier to investigate and correct. Waiting until month-end to discover a problem from three weeks ago makes finding the source much harder, especially if you process hundreds of reservations that month.

Set a consistent schedule and stick to it. Reconciliation that happens "when we have time" tends to fall behind, creating backlogs that become overwhelming.

The Role of Specialized Trust Accounting Software

Generic accounting software like QuickBooks can work for smaller portfolios, but many property managers start running into limitations once they grow beyond 10 properties. Manual reconciliations, spreadsheets, and workarounds become harder to manage as reservation volume increases.

Purpose-built trust accounting software automates the three-way reconciliation process. It tracks owner balances automatically, helps break down OTA batch deposits, and gives teams clearer visibility into reservations, payouts, expenses, and balances in one place. The bank reconciliation features connect to your accounts and suggest matches for incoming transactions.

The investment in specialized software pays off quickly through time savings and error reduction. More importantly, it gives your team a reliable system for understanding your cash inflows and outflows down to the penny.

Making Reconciliation Work for Your Business

Reconciliation isn’t the most exciting part of running a vacation rental business, but it’s one of the most important. When your numbers are accurate and up to date, owner reporting gets easier, month-end becomes less stressful, and your team spends less time chasing down discrepancies.

The vacation rental industry's transaction complexity makes reconciliation harder than traditional property management. OTA batch deposits, constant guest turnover, and property-specific expenses create a web of financial activity that requires careful tracking. But the same principles apply: match your bank to your books, match your books to your owner balances, and investigate any differences immediately.

If you're managing more than 10 properties and still relying heavily on spreadsheets or manual reconciliation processes, consider a platform designed for vacation rental trust accounting. VRTrust automates three-way reconciliation, syncs with major PMS platforms, and generates owner statements that keep everyone informed.

See how three-way reconciliation works with VRTrust →